Register now for better personalized quote!

Karl Whitelock

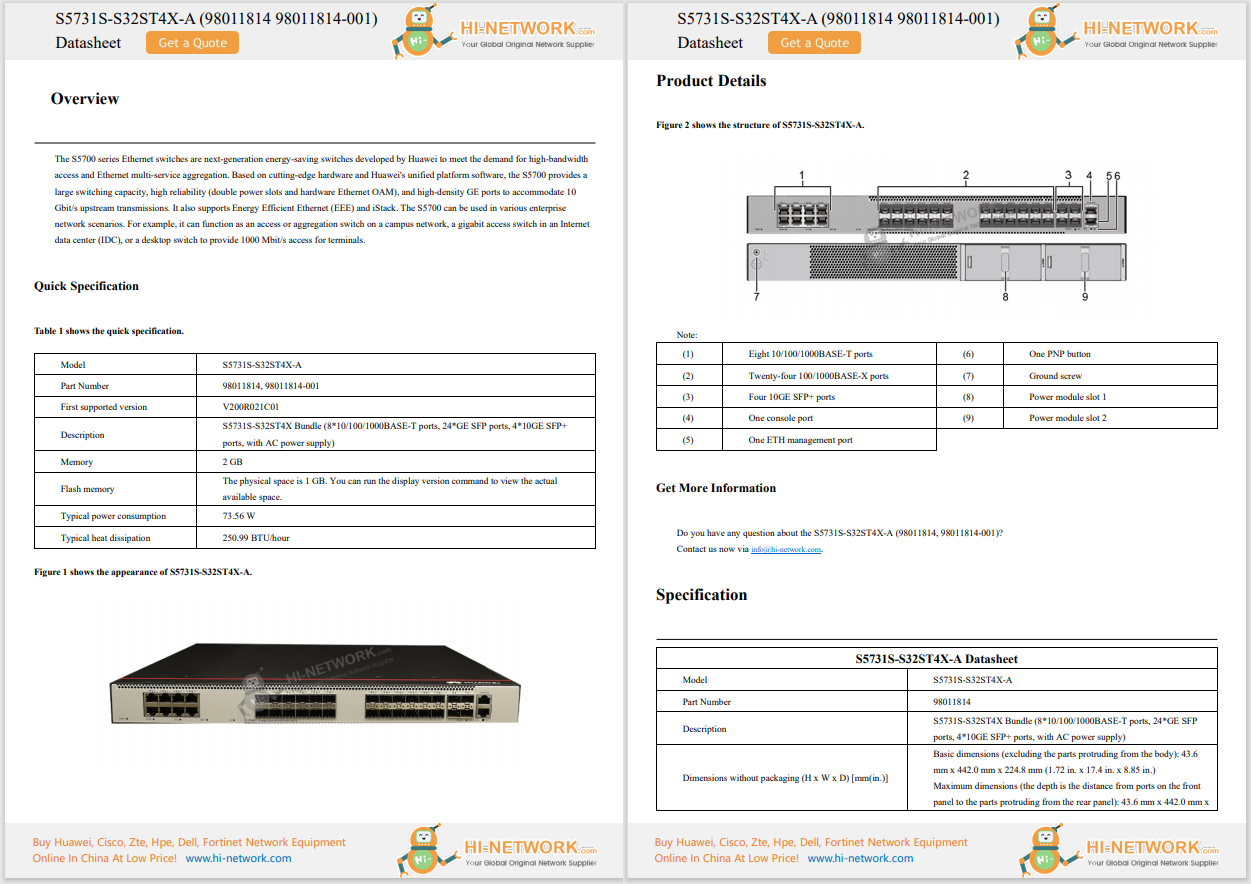

Karl WhitelockBy Karl Whitelock, Research Vice President, Communications Service Provider Operations & Monetization, IDC

Midsize and small SPs-service providers with a customer base of 1 million customers or less-have relatively small customer bases and limited technical staff. However, they possess many of the same business and operational challenges as larger operators, but their approach to executing business strategy is noticeably different from the rest of the market.

Specialization and business focus are essential actions for midsize/small SPs, as their competitive landscape is expanding. IDC estimates there are more than 3,000 midsize/small SPs globally, with the Americas region accounting for over 80% of the global market. IDC also estimates that midsize/small SP global revenue in 2020 was approximately$10.6 billion.

Recognizing the scope and complexity necessitated by the digital transformation journey of a typical service provider, IDC worked with Cisco to establish a framework that could make the journey manageable and measurable. The outcome of this effort is the SP Digital Maturity Index, which provides a guide to help service providers improve the effectiveness of their digital transformation initiatives and to show how they can measure the progress of their digital journey. The Index describes various levels of service provider digital maturity along a scale of five designations defined as:

Figure 1 shows an overall comparison of digital maturity levels for midsize/small SPs and large SPs across these five domains.

Figure 1 -Digital Maturity Measure of Midsize/Small Service Providers Versus Large Service Providers n = 401 Source: IDC's SP Digital Readiness Survey, 2021

Figure 1 -Digital Maturity Measure of Midsize/Small Service Providers Versus Large Service Providers n = 401 Source: IDC's SP Digital Readiness Survey, 2021Only a small percentage of midsize/small SPs have achieved high levels of digital maturity, while most are in the early stages of implementing new technologies, shifting from manual to automated processes, and deploying new services.

Regardless of the level of maturity that a large or midsize/small SP may possess, there are several needs that both groups are keenly aware of, and they know they must provide dedicated attention to each need. For midsize/small SPs especially, theIDC SP Digital Readiness Survey 2021report offers survey-based insight regarding many of these needs including:

Although discussion of each category of need is the purpose of theIDC SP Digital Readiness Survey, a sample containing some of the report findings is as follows:

Investment priorities and market drivers.Midsize/small SPs are facing several competitive challenges that are forcing prioritization of their strategic imperatives and investments. Much like larger operators, midsize/small SPs are focused on reducing operating costs through greater operational efficiencies. In fact, according to the survey,nearly one-third of the midsize/small SPs respondents cited improvement to operational efficiency as their top business priority (see Figure 2). Accomplishing this goal requires automation in areas where it will have the most business impact to an SP's operations. This is an important point, since the communications industry has repeatedly marketed automation as the cure-all to solving service provider operational challenges.

Figure 2 -Top Business Priorities for Midsize/Small Service Providers Q. What are the top 3 high-level business priorities for your organization? n = 201 midsize and small service providers Source: IDC's SP Digital Readiness Survey, 2021

Figure 2 -Top Business Priorities for Midsize/Small Service Providers Q. What are the top 3 high-level business priorities for your organization? n = 201 midsize and small service providers Source: IDC's SP Digital Readiness Survey, 2021IDC believes greater use of automation and analytics plays an important role in improving the customer experience, but we remain concerned about the time and effort needed to reach this goal. However, the ability to analyze and correlate various types of customer information and then use the insight gained from this data to recommend new services or upgrades to existing services is an area that many midsize/small SPs are focused on today. With a focus on improving NPS as a strategic goal and using high scores as a source of differentiation, IDC believes that midsize/small SPs can prioritize investments in customer-facing systems that generate actionable insights that will play a strategic role in improving the customer experience.

While midsize/small service providers have made solid progress toward their digital transformation goals, there remains plenty more to accomplish to reach higher levels of digital maturity. In virtually all domains studied as part of IDC'sDigital Transformation Survey, very few of the midsize/small providers surveyed have reached pioneer or deployer status. Midsize/small providers expect to make significant strides over the next two years, and this will be critical to success as the midsize/small communications segment becomes much more competitive with new providers entering the market.

Increasing competitive intensity, changing customer preferences, and rapid technological advances make digital transformation a continuous effort. For midsize/small SPs, success will be determined by the ability to transform their business model and utilize technology, data, and processes in ways that will improve operational efficiency, enhance customer experience, and drive growth through the pursuit of new revenue streams.

To learn more about the opportunities and challenges of midsize/small SPs, please join a one-hour webinar Midsize/Small SP Opportunities and Challenges on December 7, 2021 at 8:00 a.m. PST.

Hot Tags :

Digital Transformation

network

automation

Mid / Small Service Providers

IDC Research

Hot Tags :

Digital Transformation

network

automation

Mid / Small Service Providers

IDC Research

Register Email now for Weekly Promotion Stock

100% free, Unsubscribe any time!

Add 1: Room 605 6/F FA YUEN Commercial Building, 75-77 FA YUEN Street, Mongkok KL, HongKong Add 2: Room 405, Building E, MeiDu Building, Gong Shu District, Hangzhou City, Zhejiang Province, China

Whatsapp/Tel: +8618057156223 Tel: 0086 571 86729517 Tel in HK: 00852 66181601

Email: [email protected]

English

English Pусский

Pусский Français

Français Español

Español Português

Português